The Golden arches - logo of the fast food giant McDonalds Corporation - has become the omnipresent logo that jostles both urban and rural landscapes alike, all over the world.

Whether you are driving to work in your car, taking the subway, travelling across state borders on an interstate highway, taking a flight or even just leisure shopping in your neighborhood mall, you cannot escape the presence of this ubiquitous symbol, tempting you to step in and enjoy one of its lip smacking meals once again, an experience that you have come to enjoy so much while growing up through your teens. The menu changes just a little once in a while, but the experience never ever changes. Rarely if ever, will you have the opportunity to be dissatisfied with the food or the service, whether you are dining in-house or picking up from the drive-through window. Product and Service Quality is maintained to the dot and regardless of employee turnover, there is no deterioration in either one.

Whether you are driving to work in your car, taking the subway, travelling across state borders on an interstate highway, taking a flight or even just leisure shopping in your neighborhood mall, you cannot escape the presence of this ubiquitous symbol, tempting you to step in and enjoy one of its lip smacking meals once again, an experience that you have come to enjoy so much while growing up through your teens. The menu changes just a little once in a while, but the experience never ever changes. Rarely if ever, will you have the opportunity to be dissatisfied with the food or the service, whether you are dining in-house or picking up from the drive-through window. Product and Service Quality is maintained to the dot and regardless of employee turnover, there is no deterioration in either one.

Yet, the operational smoothness at the ordering counter betrays the ongoing upheaval in

the financial structure of the company. The fact is that McDonalds management has been on a stock buy-back spree for a while now. The chart alongside shows how the outstanding shares of the company is decreasing steadily over the past two years. This is because McDonalds is lapping up its own shares from the stock market using the money from its Share Capital account. Ordinarily, a share buy-back is a welcome sign because it is an indication from management that the current share price is much below its intrinsic value. While McDonalds stock has moved up about 30% in response to this move in the past two years itself, clearly the Management is not relenting and wants the stock to do much more.

the financial structure of the company. The fact is that McDonalds management has been on a stock buy-back spree for a while now. The chart alongside shows how the outstanding shares of the company is decreasing steadily over the past two years. This is because McDonalds is lapping up its own shares from the stock market using the money from its Share Capital account. Ordinarily, a share buy-back is a welcome sign because it is an indication from management that the current share price is much below its intrinsic value. While McDonalds stock has moved up about 30% in response to this move in the past two years itself, clearly the Management is not relenting and wants the stock to do much more.

As a proof of this, take a look at the NetWorth of the Company in the alongside chart over the past two years. It shows that NetWorth is declining steadily, to the extent that it is now actually negative and in the red. This implies that the Company has exhausted all its share capital in the buy-back process and is in fact now using debt to finance the share buy-back. This is an extreme step. It indicates the strong conviction of the management in its own business model, to the extent that it is relying on debt not only to finance ongoing operations but also to finance the share buy-back. Keep in mind that a negative Networth implies that the book value of the share is negative. If the company were to shut down tomorrow for any reason, the shareholders of the company would theoretically get nothing back!

As a proof of this, take a look at the NetWorth of the Company in the alongside chart over the past two years. It shows that NetWorth is declining steadily, to the extent that it is now actually negative and in the red. This implies that the Company has exhausted all its share capital in the buy-back process and is in fact now using debt to finance the share buy-back. This is an extreme step. It indicates the strong conviction of the management in its own business model, to the extent that it is relying on debt not only to finance ongoing operations but also to finance the share buy-back. Keep in mind that a negative Networth implies that the book value of the share is negative. If the company were to shut down tomorrow for any reason, the shareholders of the company would theoretically get nothing back!

It is perhaps with this thought in mind that Management has resisted the urge to stop

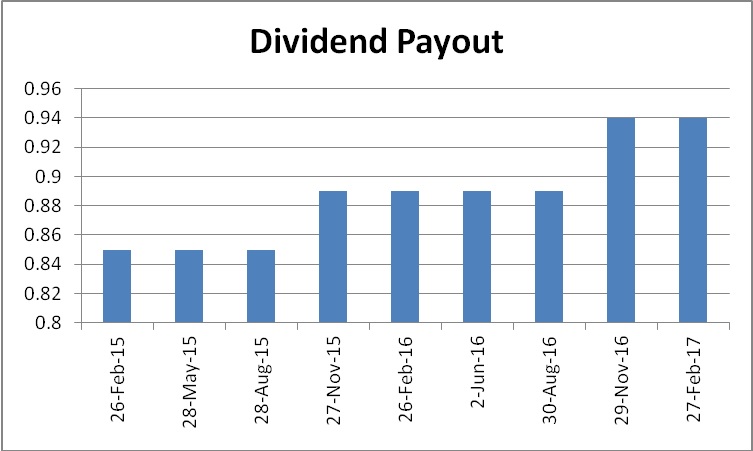

paying dividends during this entire buy-back process. The chart alongside shows that dividend payout is consistent, and is in fact increasing over time. This means that profits from existing operations are being returned to investors partly in the form of dividends, and the rest together with additional debt is being used to fund existing operations, capital expenditures and the share buy-back process.

paying dividends during this entire buy-back process. The chart alongside shows that dividend payout is consistent, and is in fact increasing over time. This means that profits from existing operations are being returned to investors partly in the form of dividends, and the rest together with additional debt is being used to fund existing operations, capital expenditures and the share buy-back process.

How bold a move is this? I have to admit it is very bold. The conviction required to make a share buy-back just once is high enough – but to sustain it consistently quarter after quarter, to the extent that NetWorth becomes negative and increase dividend payout simultaneously - requires conviction of a higher order. The management of the company believes that they have a winning formula in their business model that is unbeatable. This formula extends from the deepest link in their supply chain all the way to the ordering counter in each restaurant. Customers are assured of not only a quality meal at a reasonable price, but of a dining experience that is consistent in any McDonalds restaurant, anywhere in the world. Achieving this level of operational excellence requires time no doubt, but more importantly it requires the continuous and arduous cultivation of intangible assets - all the things that you cannot touch and feel but know for sure are the keys to your success and to your competitive advantage in the marketplace.

What does all this mean for the stock? Well for one, it has nowhere to go but up in the near and medium term. Secondly, once management feels that the stock price has reached acceptable levels, they may start re-issuing the stock to the market at a higher price. In doing so, they would have then invested in their own business with their own (and some borrowed) money and made handsome returns for the business and for each investor in the process!

So the next time you are in a McDonalds restaurant, think about this strategy at play, while you are enjoying your next happy meal along with your family!

p.s. At the time of writing this article, McDonalds stock was trading $130.76, which means the stock is up 7.4% in the first three and half months of calendar year 2017!

Yet, the operational smoothness at the ordering counter betrays the ongoing upheaval in

As a proof of this, take a look at the NetWorth of the Company in the alongside chart over the past two years. It shows that NetWorth is declining steadily, to the extent that it is now actually negative and in the red. This implies that the Company has exhausted all its share capital in the buy-back process and is in fact now using debt to finance the share buy-back. This is an extreme step. It indicates the strong conviction of the management in its own business model, to the extent that it is relying on debt not only to finance ongoing operations but also to finance the share buy-back. Keep in mind that a negative Networth implies that the book value of the share is negative. If the company were to shut down tomorrow for any reason, the shareholders of the company would theoretically get nothing back!

As a proof of this, take a look at the NetWorth of the Company in the alongside chart over the past two years. It shows that NetWorth is declining steadily, to the extent that it is now actually negative and in the red. This implies that the Company has exhausted all its share capital in the buy-back process and is in fact now using debt to finance the share buy-back. This is an extreme step. It indicates the strong conviction of the management in its own business model, to the extent that it is relying on debt not only to finance ongoing operations but also to finance the share buy-back. Keep in mind that a negative Networth implies that the book value of the share is negative. If the company were to shut down tomorrow for any reason, the shareholders of the company would theoretically get nothing back!It is perhaps with this thought in mind that Management has resisted the urge to stop

How bold a move is this? I have to admit it is very bold. The conviction required to make a share buy-back just once is high enough – but to sustain it consistently quarter after quarter, to the extent that NetWorth becomes negative and increase dividend payout simultaneously - requires conviction of a higher order. The management of the company believes that they have a winning formula in their business model that is unbeatable. This formula extends from the deepest link in their supply chain all the way to the ordering counter in each restaurant. Customers are assured of not only a quality meal at a reasonable price, but of a dining experience that is consistent in any McDonalds restaurant, anywhere in the world. Achieving this level of operational excellence requires time no doubt, but more importantly it requires the continuous and arduous cultivation of intangible assets - all the things that you cannot touch and feel but know for sure are the keys to your success and to your competitive advantage in the marketplace.

What does all this mean for the stock? Well for one, it has nowhere to go but up in the near and medium term. Secondly, once management feels that the stock price has reached acceptable levels, they may start re-issuing the stock to the market at a higher price. In doing so, they would have then invested in their own business with their own (and some borrowed) money and made handsome returns for the business and for each investor in the process!

So the next time you are in a McDonalds restaurant, think about this strategy at play, while you are enjoying your next happy meal along with your family!

p.s. At the time of writing this article, McDonalds stock was trading $130.76, which means the stock is up 7.4% in the first three and half months of calendar year 2017!